This article first appeared on World Economic Forum.

- We already have the tools to tackle global emissions, but need to find the political will to rapidly deploy them by building the teams across industry, government and finance.

- For these technological solutions to be deployed globally by 2050, they need to be commercialised and rolled out on a scale sufficient to trigger cost reductions before 2030.

- Industry and government need to jointly develop the game plan, mapping out how to reach net-zero emissions in each sector by mid-century. Playing solo is not an option!

The best of human endeavour, excellence and solidarity is currently on display at the Tokyo Olympics. In the face of the challenges posed by the COVID-19 pandemic, the Games is bringing the world together in sporting prowess and teamwork. Humanity will need to find that same level of solidarity and teamwork if we are to successfully work together to address climate change.

As with every sportsman and woman in Tokyo, we know what we need to do. We have the tools we need to tackle global emissions; we simply need to find the political will to rapidly deploy them. We need to pull together to build the teams – across industry, government and finance – to deliver decarbonisation.

Across the seven sectors on which we are focusing our activity – aviation, shipping, heavy-duty road transport, iron and steel, aluminium, concrete, and chemicals – low- and zero-carbon alternatives already exist. Whether they rely on hydrogen, ammonia, biochemicals or advanced biofuels, new technologies and production processes can, in theory, be deployed to drive emissions to zero by the middle of this century.

Going for green

The challenge is that, in pretty much every case, these alternatives are not yet commercially available, and hence are still more expensive than conventional options, often significantly so (from perhaps 20% to 200% more). This ‘green premium’, as identified by Bill Gates, makes it difficult for many businesses to invest today, even if doing so could give them a competitive edge over their rivals as the net-zero economy emerges over the coming decades.

The good news, though, is that even if significant at a business-to-business level, this green premium would have a low impact on consumer prices (of less than 1%) once passed through the whole value chain. Indeed, this figure will fall further with scale and learning-curve effects.

We are now in a race against time: for these technological solutions to be deployed globally and become the “new normal” by 2050, they need to be commercialised and rolled out on an initial scale sufficient to trigger cost reductions before 2030.

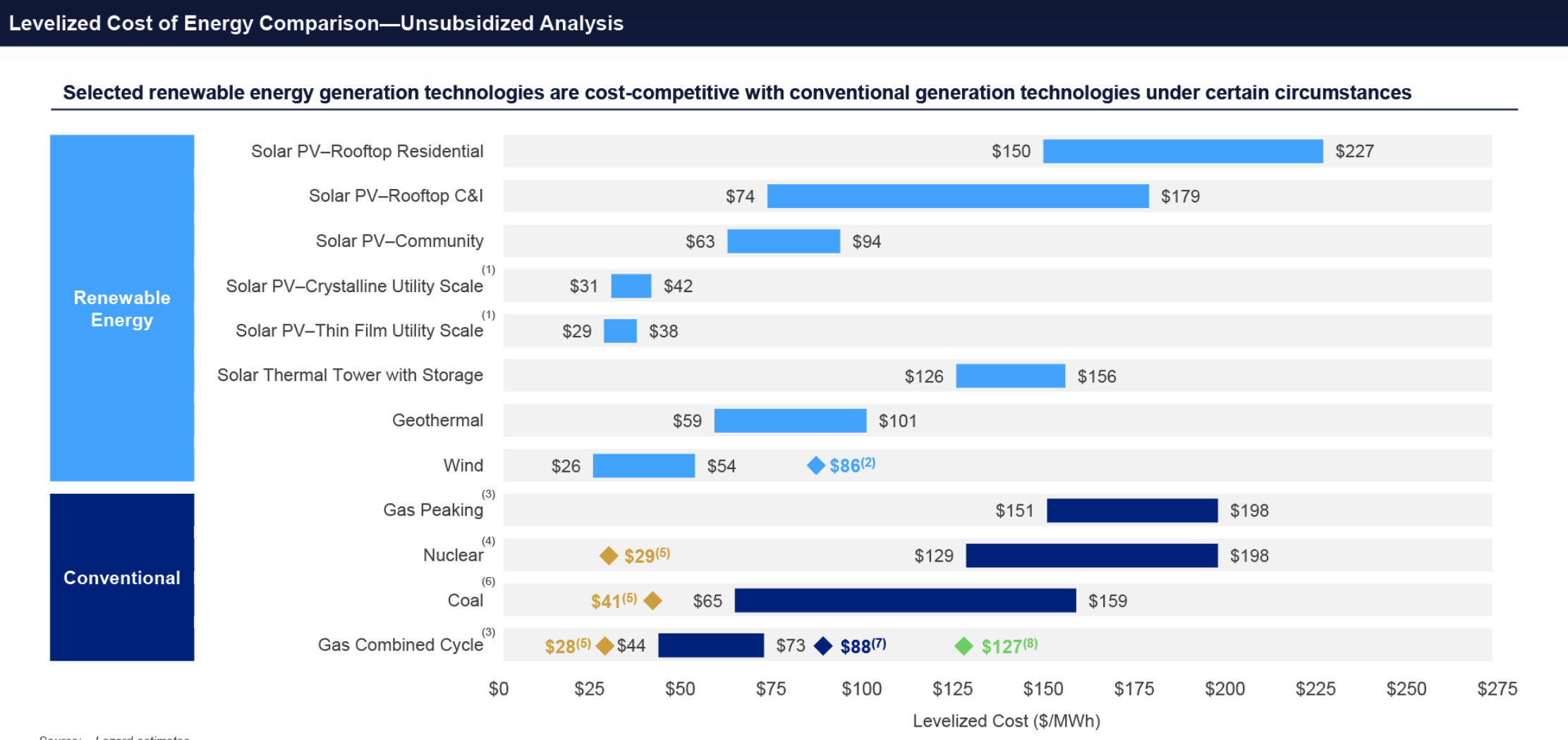

Fortunately, we have a successful case study of how to do just that in the dramatic growth of renewable energy of the last three decades. Over the past 10 years, wind and solar have grown rapidly (fourfold and more than 17 times, respectively) while their costs have fallen precipitously. According to figures from the investment bank Lazard, the cost of wind power fell by 71% between 2009 and 2020, and utility-scale solar by 90%.

The reason is straightforward. Using auctions, tax breaks, generation subsidies and green certificate schemes, governments initially underwrote the green premium in clean energy, allowing more expensive wind and solar power to compete with power sourced from coal, nuclear and natural gas-fired generators.

By subsidising early markets for renewable electricity and guaranteeing stability in revenues, governments encouraged massive investment in clean energy technology and in large-scale manufacturing. In many jurisdictions, it is now cheaper to install new solar farms than it is to run existing coal-fired power plants.

Training for success

This is an extraordinary achievement. But it didn’t happen overnight. Denmark first introduced subsidies for wind farms in 1981, while Germany’s feed-in tariff programme dates back to 1991. We can’t afford to spend three decades bringing down the cost of green hydrogen production, ammonia for the shipping sector, or biochemicals and synthetic fuels. Nor do we have to, because we have learned how to use policy tools to accelerate such transitions.

However, these policy tools will need to be tailored to the realities of the carbon-intensive industries. Two key differences make the story for harder-to-abate sectors less straightforward:

1. Unlike with renewables and power generation, there is no single-bullet solution to decarbonise those sectors: in heavy industry, several low-carbon technology options will co-exist, as their cost-competitiveness will vary by region and even by plant. In the mobility sectors, different technologies are likely to cater for different journey lengths, with shorter journeys being electrified and longer journeys continuing to rely on liquid fuels. The multiplicity of solutions makes it more complex to develop policy tools that will meet all needs.

2. Those sectors operate across national borders. A tightening of national targets and obligations, even if supported by subsidy mechanisms, will still likely trigger an increase in carbon costs for companies in those sectors, which could penalise them vis-à-vis their international competitors. This carbon leakage issue demands innovative forms of international cooperation.

Playing as a team

This is why decarbonisation is a team sport. Industry, finance and government need to play as a team to win against climate change. Industry and government need to jointly develop the game plan, mapping out how to reach net-zero emissions in each sector by mid-century, and agreeing on the best technology and business model solutions (or, most likely, portfolio of solutions) to pursue. Then they need to play together to create the end-markets that the private sector will need to justify investment in innovation, manufacturing and deployment.

This requires nothing less than:

- Unprecedented public-private partnerships to de-risk private investment through regulations and public finance mobilisation;

- Innovative public-public cooperation (sector-specific groups of governments agreeing on joint action, collaborating on R&D and progressing toward a global level playing field, as well as vertical cooperation between federal and decentralised governments);

- New forms of private-private cooperation across the value chain, from energy providers to consumer good companies, to demonstrate the feasibility of green value chains, and sometimes even between competitors to speak with one voice to governments and financial institutions.

In the race against climate change, playing solo is not an option! Aviation

As other sectors proceed to decarbonize, the aviation sector could account for a much higher share of global greenhouse gas emissions by mid-century than its 2%-3% share today.

Sustainable aviation fuels (SAF) can reduce the life-cycle carbon footprint of aviation fuel by up to 80%, but they currently make up less than 0.1% of total aviation fuel consumption. Enabling a shift from fossil fuels to SAFs will require a significant increase in production, which is a costly investment.

The Forum’s Clean Skies for Tomorrow (CST) Coalition is a global initiative driving the transition to sustainable aviation fuels as part of the aviation industry’s ambitious efforts to achieve carbon-neutral flying.

The coalition brings together government leaders, climate experts and CEOs from aviation, energy, finance and other sectors who agree on the urgent need to help the aviation industry reach net-zero carbon emissions by 2050.

The coalition aims to advance the commercial scale of viable production of sustainable low-carbon aviation fuels (bio and synthetic) for broad adoption in the industry by 2030. Initiatives include a mechanism for aggregating demand for carbon-neutral flying, a co-investment vehicle and geographically specific value-chain industry blueprints.

The shipping sector provides an example of how such a team can work together. More than 150 companies have joined the Getting To Zero Coalition, pledging to introduce zero-emission shipping in deep-sea lanes on a commercial basis by 2030. They come from all corners of the world, and represent shippers, freight forwarders, ship builders, fuel and bunkering service providers, cargo owners, financial institutions, and governments of countries with a large maritime sector.

They are now developing a net-zero transition strategy, which will lay out the solutions and fuels to be used to reduce emissions faster than International Maritime Organization targets currently suggest. In parallel, they are working together to sail the very first zero-emission ships in the next few years, building consortiums with fuel providers, port authorities and shippers, bringing in cargo owners ready to pay a premium for green shipping, and securing public and private financing.

This is an enterprise beyond the scope of even the largest shipping giant – and, indeed, of the shipping sector as a whole. It takes collaboration with the energy sector, but also with the many sectors which ship goods around the world. And, in the short to medium term, it will take government support to accelerate R&D, de-risk investment in the fuel supply chain, new port infrastructure, new ships and engines, and stimulate demand for green shipping via regulation and mandates.

All of that can be done while adding less than 1% to consumer prices of goods shipped around the world. We, as consumers, need to be ready to pay that small price. The maritime team needs us to make that pass to score against climate change.

Written by:

Faustine Delasalle, Co-Executive Director, Mission Possible Partnership and Director, Energy Transitions Commission

Anthony Hobley, Co-Executive Director, Mission Possible Partnership and an Executive Fellow, WEF, World Economic Forum